HOW MUCH TO SAVE FOR RETIREMENT

Tracking your progress toward any goal has never been easier, thanks to the plethora of apps available today. You can monitor your steps, track packages, manage your diet, and even keep tabs on your family's whereabouts. However, one area that often gets overlooked is tracking your progress toward saving for retirement. How much attention do you pay to your retirement savings, and when should you start?

The Importance of Early and Steady Retirement Planning

Retirement planning can be daunting, especially early in your career. With retirement seeming so far away, it's challenging to prioritize saving for it amid present-day financial obligations. You might have student loans, be saving for a home, or setting aside money for your children’s college education. Despite these competing priorities, it's crucial to make consistent progress in your retirement savings, no matter your age. Regularly assessing where you stand can help you plan more effectively and with greater intention.

Why Now Is the Right Time to Review Your Portfolio

Market volatility, significant life changes, and rising living costs can all affect your investment strategy. Regularly reviewing your portfolio can help you better align your current financial situation with your long-term goals.

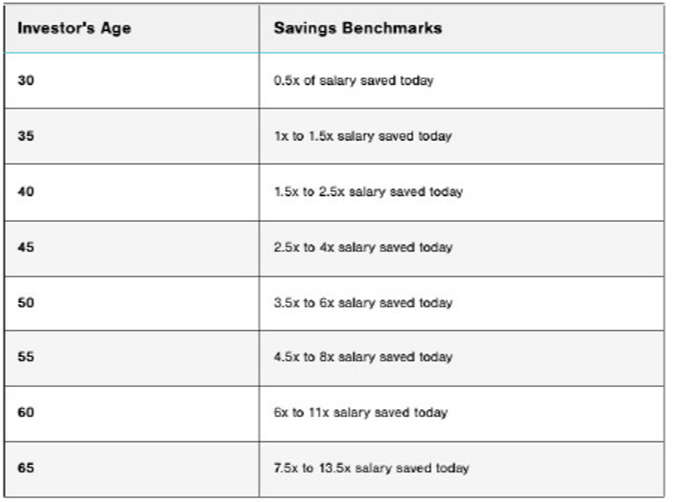

What Should You Have Saved by Age 35, 50, and 60?

Research indicates that people often rely on rough estimates or rules of thumb for financial decisions. Recognizing this, many financial firms publish savings benchmarks that suggest ideal savings levels at different ages relative to an individual’s income. These benchmarks are not a substitute for planning your finances but offer a quick way to assess if you're on track. They are certainly better than guessing and can prompt action toward improving savings.

Realistic and Achievable Benchmarks

For benchmarks to be helpful, they must be realistic. If targets are set too low, they can create a false sense of security. Conversely, overly ambitious targets can be discouraging. After analyzing various targets, we have developed a set of achievable benchmarks. We began with the end goal in mind: determining the necessary assets by age 65, primarily influenced by income. Higher earners, who receive a smaller proportion of their income from Social Security, typically need more assets relative to their income.

Benchmark provided by FMeX

We suggest that most people aiming to retire around age 65 should accumulate assets equivalent to 7½ to 13½ times their preretirement gross income. From this target, we derived benchmarks for other ages, assuming a reasonable earnings and savings trajectory. Instead of assuming immediate saving of 15% of income from the first paycheck, our model starts with a 6% savings rate at age 25, increasing by one percentage point each year until reaching an appropriate level.

Savings Benchmarks by Age

- By Age 35: Aim to have saved 1 to 1½ times your annual income.

- By Age 50: Target 3 to 6 times your annual income in savings.

- By Age 60: Strive to have 6 to 11 times your annual income saved.

These benchmarks are designed to be attainable, encouraging steady savings growth throughout your career. Higher earners should consider aiming beyond the 15% savings rate to ensure adequate retirement funds.

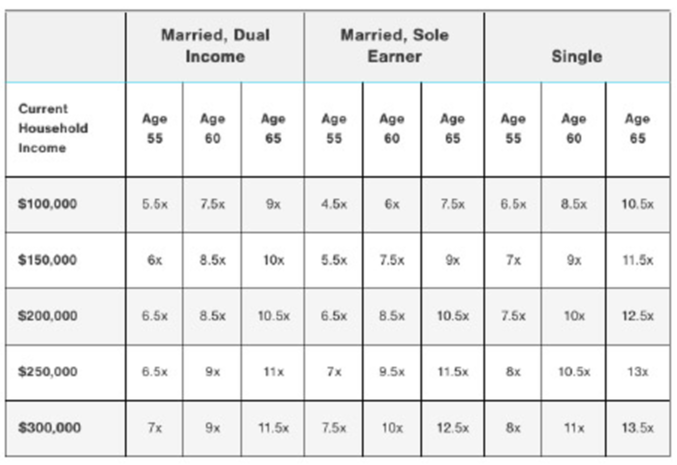

A Closer Look at Savings Benchmarks Later in Your Career

Benchmark provided by FMeX

Assumptions: See "Savings Benchmarks by Age—As a Multiple of Income" above. "Dual income" means that one spouse generates 75% of the income that the other spouse earns.

Take Action Now

Regardless of your age, the best time to start saving for retirement is now. Reviewing your portfolio and adjusting your savings strategy can help you stay on track with your retirement goals. If you're uncertain about your progress, consider seeking a portfolio review to gain clarity and direction.

Get a Portfolio Review

Market uncertainty and life changes can impact your investment strategy. A portfolio review can provide personalized insights to help you stay on track for retirement. By staying informed and proactive, you can work towards building a robust retirement plan that will support you in your golden years.

HOW DOES MARRIAGE AFFECT YOUR RETIREMENT PLANS?

Marriage is about more than just a wedding. As you dream about your future home, family, and travels, it's also essential to discuss your retirement plans and how to pursue them together.

According to the U.S. Census Bureau, the median age for a first marriage is 30.5 for men and 28.6 for women. This means many couples today enter marriage with some working years behind them, often bringing prior retirement savings and possibly debt into the relationship.

The Impact of Combining Finances

One of the most complex aspects of merging lives with a significant other is combining finances. Many couples bring debt into the marriage, and managing this while planning for the future can be challenging. Open and honest communication is crucial to ease this transition. Discuss your financial history, current obligations, and future goals to create a unified approach to your finances.

Addressing Retirement Planning Hurdles

Couples often face significant challenges in retirement planning, such as budgeting, spending habits, individual risk tolerances, and overall goals. Here are some steps to help navigate these hurdles:

- Budgeting Together:

- Start with a joint budget to understand your combined income and expenses.

- Identify areas where you can save more or cut unnecessary spending.

- Allocate funds for retirement savings as a priority.

- Understanding Spending Habits:

- Discuss each other's spending habits and find common ground.

- Establish guidelines for discretionary spending to avoid conflicts.

- Consider setting up individual accounts for personal spending, alongside a joint account for shared expenses.

- Aligning Risk Tolerances:

- Evaluate each other's risk tolerance and investment preferences.

- Develop a diversified investment strategy that balances your risk profiles.

- Revisit your investment strategy periodically to help it better align with your goals.

- Setting Common Goals:

- Define your retirement vision together—where you want to live, how you want to spend your time, and what lifestyle you envision.

- Set short-term and long-term financial goals to work toward this vision.

- Regularly review your progress and adjust your plans as needed.

Social Security and Retirement Benefits

Marriage also affects your eligibility and strategy for claiming Social Security and other retirement benefits:

- Spousal Benefits: You may be eligible for spousal benefits, which can be up to 50% of your spouse's Social Security benefit.

- Survivor Benefits: If one spouse passes away, the surviving spouse may be eligible for survivor benefits.

- Timing of Claims: Coordinate the timing of your Social Security claims to maximize your combined benefits.

Planning for Healthcare and Long-Term Care

Healthcare costs can significantly impact your retirement savings. As a couple, consider:

- Health Insurance: Evaluate your options for employer-provided health insurance or individual plans.

- Long-Term Care Insurance: Discuss the potential need for long-term care insurance to preserve your assets and ensure quality care.

Take Action Together

Successful retirement planning as a couple requires ongoing communication and collaboration. Start by having open conversations about your finances, goals, and retirement vision. Use these discussions to build a comprehensive plan that reflects both of your needs and aspirations.

Get Professional Advice: Consider consulting a financial professional to help you navigate the complexities of combining finances and planning for retirement. A financial professional may provide personalized guidance and strategies to help you stay on track as you work toward your retirement goals.

Marriage marks the beginning of a new chapter in your life. By planning and working together, you can build a financially secure future and enjoy a fulfilling retirement.

Planning for retirement as a couple can be complex, but with open communication and a solid strategy, you can achieve your dreams together. Start the conversation today and take the first step towards a secure and happy retirement.

THE 80/20 RULE OF THUMB FOR RETIREMENT (PARETO PRINCIPLE)

A recent survey by Bankrate revealed that 52% of Americans feel their retirement savings won't sustain them through their retirement years. This sentiment often stems from late starts in saving, early withdrawals, or inconsistent saving habits. While there isn't a strict formula for saving and budgeting, the 80/20 rule is a simple yet effective guideline that can aid in retirement planning, no matter when you start saving.

Understanding the 80/20 Rule

The 80/20 rule, also known as the Pareto Principle, states that 80% of effects come from 20% of causes. In the context of retirement savings, this principle suggests that a small portion of your financial habits will significantly impact your overall retirement savings. Applying this rule can help you focus on the most effective strategies to maximize your retirement funds.

How to Apply the 80/20 Rule to Your Retirement Savings

- Prioritize High-Impact Savings:

- Identify the key actions that will have the most significant impact on your retirement savings. This might include contributing to employer-sponsored retirement plans like a 401(k) or opening an IRA.

- Automate your savings to ensure consistent contributions. Even small, regular deposits can grow substantially over time due to compound interest.

- Focus on Reducing High-Impact Expenses:

- Review your spending habits and identify areas where you can cut costs without sacrificing your quality of life. Focus on the 20% of expenses that make up 80% of your unnecessary spending.

- Redirect the savings from reduced expenses directly into your retirement accounts.

- Maximize Employer Contributions:

- Take full advantage of any employer matching contributions to your retirement plan. This is essentially free money that can significantly boost your savings

- Ensure you contribute at least enough to get the full match from your employer.

- Invest Wisely:

- Focus on investment choices that offer the best returns relative to their risk. Diversified, low-cost index funds or target-date funds can be excellent options for long-term growth.

- Regularly review and adjust your investment portfolio to align with your retirement goals and risk tolerance.

- Leverage Tax-Advantaged Accounts:

- Maximize contributions to tax-advantaged retirement accounts like 401(k)s and IRAs. These accounts offer tax benefits that may enhance your savings.

- Consider Roth accounts for tax-free growth and withdrawals in retirement

- Avoid Early Withdrawals:

- Resist the temptation to withdraw from your retirement savings early. Early withdrawals not only reduce your principal but can also result in penalties and lost growth potential.

- Establish an emergency fund to cover unexpected expenses, so you don't have to dip into your retirement savings prematurely.

Example of the 80/20 Rule in Action

Imagine you have identified that dining out and entertainment account for 20% of your expenses but 80% of your discretionary spending. By reducing these expenses, you could free up a significant amount of money to contribute to your retirement savings.

Similarly, focusing on maximizing contributions to your retirement accounts and ensuring you get the full employer match can make a substantial difference in your retirement nest egg. Even if these actions only represent a small portion of your overall financial activities, they can drive the majority of your progress toward your retirement goals.

Start Applying the 80/20 Rule Today

No matter where you are in your retirement planning journey, applying the 80/20 rule can help you focus on the most impactful actions to build your retirement savings. By prioritizing high-impact savings strategies, reducing unnecessary expenses, and leveraging employer contributions and tax advantages, you can significantly enhance your financial confidence in retirement.

Take Action: Begin by identifying the 20% of actions that will drive 80% of your retirement savings success. Make these actions a priority and incorporate them into your financial routine. Over time, these focused efforts can lead to substantial improvements in your retirement readiness.

Applying the 80/20 rule to your retirement savings strategy can simplify your planning process and help you work toward making impactful financial decisions. Start today and take the first step towards a more secure and fulfilling retirement.

YOUR FINANCIAL PROFESSIONAL

Financial professionals can play a crucial role in guiding individuals towards their financial goals, providing expertise and experience that may significantly impact long-term financial stability. One of the key benefits of working with a financial professional is their ability to help you determine how much to save for retirement. They may do this by analyzing your current financial situation, projected future earnings, and lifestyle goals. This comprehensive assessment can allow them to create an appropriate savings plan that takes into account various factors such as inflation, investment returns, and expected retirement age. By having a clear and realistic savings target, you can make informed decisions about your spending and investment strategies to help you work toward having enough funds to enjoy a comfortable retirement.

Marriage can significantly impact your retirement planning, and a financial professional can help you navigate these changes effectively. Financial professionals consider the combined income, expenses, and retirement accounts of both partners, allowing for a coordinated and efficient strategy. They can also help address potential changes in benefits, such as Social Security and pensions, and the implications of spousal contributions and distributions. Additionally, a financial professional may apply the 80/20 rule (Pareto Principle) to retirement planning, which suggests that 80% of the effects come from 20% of the causes. In the context of retirement, this principle may potentially help identify investments or decisions that may have the most significant impact on your retirement savings. By focusing on the most influential factors, a financial professional can work toward enhancing your retirement plan, helping you decide how to allocate your resources effectively to pursue your desired outcomes.

Important Disclosures

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual. To determine which investment(s) may be appropriate for you, consult your financial professional prior to investing.

Investing involves risks including possible loss of principal. No investment strategy or risk management technique can guarantee return or eliminate risk in all market environments.

There is no guarantee that a diversified portfolio will enhance overall returns or outperform a non-diversified portfolio. Diversification does not protect against market risk.

Although exchange traded funds are designed to provide investment results that generally correspond to the price and yield performance of their respective underlying indexes, the trusts may not be able to exactly replicate the performance of the indexes because of trust expenses and other factors.

The principal value of a target fund is not guaranteed at any time, including at the target date.

Contributions to a traditional IRA may be tax deductible in the contribution year, with current income tax due at withdrawal. Withdrawals prior to age 59 ½ may result in a 10% IRS penalty tax in addition to current income tax.

The Roth IRA offers tax deferral on any earnings in the account. Withdrawals from the account may be tax free, as long as they are considered qualified. Limitations and restrictions may apply. Withdrawals prior to age 59 ½ or prior to the account being opened for 5 years, whichever is later, may result in a 10% IRS penalty tax. Future tax laws can change at any time and may impact the benefits of Roth IRAs. Their tax treatment may change.

This article was prepared by FMeX.

LPL Tracking #582740